Reitmans: Over 50% Upside On Plus-Sized Lingerie And Athleisure Wear

January 2, 2016 by admin

Filed under Latest Lingerie News

Summary

Reitmans is one of the cheapest retailers trading at 2x EBITDA, below TBV and 60% of its market capitalization in cash.

Strong following in plus size lingerie with the Ashley Graham collection. Additional upside from Hyba, Reitmans’s new athleisure wear brand.

Abandoned by Canadian investors due to a dividend cut and poor retail environment.

Author Update

Dec. 6, 2015, 12:25 AM

Reitmans reported its 3Q results last night. Key takeaways are as follows:

- Sales were up 80 bps YoY which was very strong considering RET has closed over ~60 Smartset stores over the period.

- Same store sales were better than expected, coming in at 7.6%, with a 4.8% increase in physical stores, the best comp in years. Furthermore we saw an acceleration in e-commerce sales. Both items correlate with physical traffic we witnessed as well as GT data.

- The company released November SSS, which was a monster 9.1% driven by a 5.5% increase in stores, an acceleration from Q3.

- Gross margins more or less came in where we expected them, at ~57.4%, however down significantly YoY. Roughly 60% of the decrease in gross margin were derived from FX. Moreover, we believe there is some margin drag from Smartset store closures as Management liquidates that concept. Assuming margins remain, we expect 1/31/16 full year EBITDA between $50MM to $55MM, implying a 2x EBITDA multiple.

- Cash flow from ops was down YoY, however we expect some of this to reverse as Q4 is one of their highest cash balance quarters.

- We continue to like the set-up as Reitmans is underfollowed and generally disliked. While retailing is a mediocre to crappy business, RET continues to have catalysts particularly for 4Q which includes upside from Hyba as well as roll-out of Ashley Graham lingerie and clothing in Lord Taylor USA/Nordstroms. Finally we are getting paid to wait with a ~5% dividend yield.

(Editors’ notes: Figures listed are in CAD unless otherwise mentioned).

Reitmans Canada, Inc. (OTCPK:RTMAF) (“Reitmans,” “RET” or the “Company”) is the largest Canadian women’s specialty retailer in Canada, operating 815 stores across 6 brand names. Reitmans represents an attractive long opportunity as the market is overlooking a cash generative business in midst of a turnaround.

Reitmans’s equity has fallen out of favor with Canadian institutional investors as demonstrated by its 50% year to date decline. Due to unfavorable FX movements between the CAD and the USD, Reitmans has felt significant impact to its margins yet these headwinds should subside over time due to better hedging practices, price adjustments and USD/CAD normalization.

Canadian institutional investors also are overly focused on the lack of top line growth and poor historic same store sales, overlooking two free call options: (1) the roll-out of its Hyba athletic wear brand in Canada and (2) continued success of Addition Elle lingerie (backed by plus sized model Ashley Graham) and roll-out of Addition Elle within Lord Taylor in the United States.

As Reitmans exits its turnaround with a smaller yet more efficient store fleet and assuming no further degradation of the business, RET offers an asymmetric return profile of 40% to 100% versus downside of ~20% at the current price.

A long position in Reitmans is merited by the following:

Attractive Valuation: Reitmans currently trades for 2.0x LTM EBITDA, at a 15% discount to tangible book value and at a ~24% LTM EV to FCF yield. This is an undemanding multiple for a business, which has generated positive free cash flow and EBITDA. This low multiple ascribes no value to Reitmans growing its Hyba brand, valuable plus sized lingerie business or partnership with Lord Taylor and other retailers.

Furthermore, recent transactions in the retailing space (particularly women’s fashion) have been consummated at multiples ranging from 7.0x to 9.0x EBITDA. To highlight on a recent example, ANN Inc. (NYSE:ANN) was recently purchased by Ascena Retail Group Inc. (NASDAQ:ASNA) for ~8.5x EBITDA while carrying a similar SSS profile. While in the current retail environment, particularly Canada, Reitmans won’t be bought out at 8x, we believe the founding family could easily take RET private at 4x to 4.5x EBITDA, simply by utilizing a turn of leverage and rolling over their equity stake or partner with Prem Watsa.

Competitive Positioning: Reitmans is the largest women’s specialty retailer across Canada with multiple store formats, 75 plus years of history, particularly in women’s value fashion and plus-sizes. The plus-sized and maternity categories are particularly attractive as they face limited pure-play competition and wider inventory selection versus department stores. RET’s brands are private label which allows for RET to maintain competitive prices while having higher quality items than Wal-Mart (NYSE:WMT), Hudson’s Bay (OTC:HBAYF) or other department store peers.

Note certain bears believe entry by U.S. brands and new plus sized entrants such as Torrid will provide a considerable headwind to Reitmans’s plus sized brands. Our channel checks and Canadian mall sleuthing revealed an entirely different target customer and product as Torrid is akin to a Rue21/HM, versus Addition Elle which tends to be higher quality and at a higher price point. The low-end on the plus size category is also competitive as Torrid will face competition from HM and Forever 21.

Improving Top line Momentum: After five years of consecutive SSS declines, SSS turned positive in FY15 as the Company benefited from a repositioning of its e-commerce division and greater productivity from its smaller store base. Further improvement should translate into improved EBITDA margins, which currently are at an all-time trough of ~7% versus the previous peak of ~17%. Going forward ~8% to 10% EBITDA margins appear to be attainable although not modeled in our base case. Margin expansion will likely come from top line stabilization or growth, FX pressures to decrease, further cost cuts and upside from Addition Elle or Hyba. However, even with flat margins and flat sales, Reitmans’s equity is highly attractive.

Moreover, we expect SSS to continue to uptick driven by the weak Canadian. While a weak CAD impacts margins, it boosts Canadian SSS as Canadian consumers are inclined to spend in Canada versus crossing the border to purchase items.

Reitmans’s e-commerce platform has been a success to date, with revenue growth accelerating throughout the year from ~40% to over 90%, which correlates with positive Google Trends traffic. Note e-commerce carries higher margins due to lower rent expense and labor.

Insider Ownership: The Reitman founding family continues to own an ~18% stake in the Company, as well as hold majority voting control. The family has been fairly conservative stewards of the business maintaining a strong, overcapitalized balance sheet and cutting costs from their bloated cost structure after facing significant top line pressures. Fairfax Financial also owns a ~13% stake and in the past have supported take-private of family owned entities.

Strong Balance Sheet: Reitmans boasts a strong balance sheet with $169MM of net cash or ~60% of its market capitalization. RET’s financial position has allowed the Company to weather heightened competition over the past four years as well as provide flexibility to execute on its turnaround plans.

Free Cash Generation: More telling, over the past four years Reitmans has generated $300MM of cash flow from operations, which has been either re-invested in the business or distributed as dividends. As same store sales comps and EBITDA margins improve, free cash flow generation will undoubtedly grow.

Furthermore, the Company closed ~34 Smart Set stores thus far at the beginning of Q3. Assuming average inventory per store of $0.8MM to $1.0MM, this could lead to an incremental ~$30MM of cash unlocked in 3Q before wind-down expenses for the concept. Reitmans will look to close its remaining 34 Smart Set stores by year-end.

Competition Exiting: Reitmans is a prime beneficiary by Target Canada’s exit (NYSE:TGT), Gap’s (NYSE:GPS) store closures as well as Sears Canada’s (SRSS) continued decline. Core brands from abroad such as Jones New York has faced significant pressure and Mexx have also left Canada, which is perceived as a fickle market. Smaller niche competitors also are floundering, with women’s retailer (also participating in plus size), Laura’s Shoppes and Melanie recently filing for bankruptcy. While the competitive landscape continues to be brutal for Reitmans over the past five years, it is poised to improve as companies such as Reitmans benefits as being one of the “homegrown” survivors.

Low Expectations Create a Favorable Setup: Reitmans’s equity is universally disliked amongst the Canadian institutional community as seen by sell-side reports (covered only by CIBC/BMO both rated “market perform”) as well as discussions with Canadian institutions. Many were previously burned by the dividend cut a few years back and lack of top line growth. Any sign of life and Reitmans equity will likely re-rate.

Why Does this Opportunity Exist?

A long opportunity in Reitmans’s common equity is available due to the following:

Dividend Reduction: In FY13, RET cut its dividend from $52MM to its current run rate of $13MM per annum. This led to a key Canadian index deletion and negative sentiment in Canada for which the institutional community places strong emphasis on dividends. While it is unlikely for RET’s dividend to be increased to $50MM in the near term, as financial performance improves, RET will likely increase its dividend in tandem.

Declining SSS: Same store sales have been meager, declining three years sequentially. In FY15 and 1Q16, same store sales have remained positive as Reitmans right sizes their store base.

FX Headwinds Margin Pressure: RET purchases its inventory from Asia in US dollars and then sells its inventory denominated in Canadian dollars (i.e. COGS in USD and sales in CAD). The decline of the Canadian dollar versus the US dollar has had a negative impact on gross margins, which have declined from ~65% in FY09 to a staggering 55% for the last quarter. Management currently hedges 60% of its FX exposure yet a 1% move in the Canadian dollar is expected to have a $0.5MM impact on operating income.

Moreover, their hedging program was incomplete during 2Q15 for which gross margins declined to 55% from 59.5% the prior, with ~60% of the impact derived from FX movement. Excluding FX, gross margins would have been ~58.3%. While due to the lack of disclosure, we have little ability to forecast gross margins for the next two quarters, we believe over the next two years they should normalize.

Low Float Out of Favor: Reitmans is a Canadian small cap retailer, with low float due to high insider ownership and Fairfax’s stake. Moreover, it has been orphaned by Canadian institutional investors due to the lack of top line growth, a similar phenomenon seen with Imvescor.

Additionally, it was rumored Reitmans was looking at potential alternatives such as a sale a couple of years ago. While obviously that process failed, we’d argue that it was much harder to sell the business at ~8x EBITDA yet at 2x EBITDA it’s materially easier to make a case that it sells for 3x or 4x EBITDA.

Poor Canadian Consumer Outlook: The outlook for the Canadian consumer is bleak, as consumer debt levels are at an all-time high and Western Canada ex. British Columbia is definitely in a recession. This potential risk could be partially hedged out through a short position in a Canadian retailer such as Sears Canada or a handful of Canadian retailers and mall REITs. Moreover, with this overhang and given it’s a retail stock, position sizing plays a big role (i.e. never size retailers large).

No Formal Investor Relations: While it is easy to access Jeremy Reitman, the Company doesn’t participate in conferences, holds no quarterly calls and has no formal presentation, etc. If the Company provides better granularity, has an actual IR outreach or investor day, institutional investors will likely come back to the story.

Business Overview

Founded in 1926 by the Reitman family, Reitmans is Canada’s largest retailer of women’s apparel and accessories with 815 stores across six banners. The largest is Reitmans, which sells to a broad demographic. The Company also has a strong market position in the plus-size and maternity segments. RET has roughly a 4% market share of Canada’s $27 billion apparel market

Store Banners

Reitman: The Reitman’s brand operates 333 stores averaging about 4,600 square feet and is Canada’s largest women’s apparel specialty chain and leading fashion brand. The brand can be seen as a comparable to Express or the Limited, while also catering to the plus sized category (to a certain extent). Note Reitmans recently signed Megan Markle as one of their spokespeople.

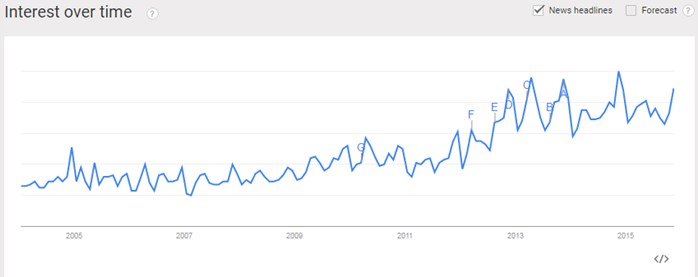

Per the below Google Trends data, traffic for Reitmans continues to increase, coinciding with the SSS increases. Notably, we also view similar trends with a consistent increase in Facebook “likes” and Twitter followers over the past three months. For example, Facebook followers have increased by ~4% per month.

Source: Google Trends Facebook

Penningtons: Penningtons operates 135 stores and is a leader in the Canadian plus size market, with fashionable merchandise and affordable quality for plus size fashion sizes 14 to 32. Penningtons operates in power centers across Canada with stores averaging about 6,000 square feet. Penningtons’ clothing is similar to Addition Elle yet at a cheaper price point and does not carry the popular Ashley Graham lingerie.

Source: Google Trends Facebook

Addition Elle: Addition Elle is a fashion destination for plus size women with a focus on fashion, quality, and fit, with the latest fashion trends. Addition Elle operates 107 stores averaging about 6,000 square feet in major malls and power centers nationwide across Canada.

Management noted the Company’s plus sized brands (Addition Elle and Penningtons) are showing strong momentum, likely due to Addition Elle’s strong performance. Furthermore, in August, it was announced Addition Elle will launch a store within a store concept in select Lord Taylor stores in the United States. Furthermore, Nordstrom (NYSE:JWN) will continue to roll out Addition Elle/Ashley Graham intimate wear. The segment has seen success by partnering with plus size models such as Ashley Graham and plus sized fashion bloggers such as Nadia Abdelhosn, who has previously done collaborations with J.C. Penny (NYSE:JCP) and other brands (over 300K followers). Per profiles on LinkedIn, this segment generates ~$145MM of revenues or 18% of sales and store revenues range from ~$1.3MM to $2.0MM. We believe Addition Elle also generates above average EBITDA and margins.

{kind=link}

Source: Google Trends Facebook

- Followers have grown by ~8% over the past 1.5 months despite flattish traffic. Twitter traffic also strong, likely due to association with Ashley Graham and Nadia Abdelhosn.

RWCO: This banner operates 80 stores averaging 4,500 square feet in premium locations in major shopping malls across Canada. RWCO is a lifestyle brand, which caters to men and women with an urban focus. RWCO can be viewed as a direct competitor to Express. Notable sponsorship includes Montreal Canadian hockey player P.K. Subban.

Source: Google Trends Facebook

Thyme Maternity: Thyme Maternity is Canada’s leading fashion brand for modern moms-to-be offering current styles from casual to work and a complete line of nursing fashion and accessories. Thyme operates 69 stores averaging 2,300 square feet in major malls and power centers across Canada as well as 21 shop-in-shop boutiques in Babies “R” Us locations in Canada. GT trends have been flattish while FB and Twitter have improved. Note USA peer Destination Maternity (NASDAQ:DEST) has no Facebook page and low Twitter followers. Thyme Maternity can be viewed as a niche cash cow brand.

Source: Google Trends Facebook

Smart Set: Smart Set offers stylish wear-to-work separate items, denims, essentials, and accessories with a greater focus on the junior’s category. Smart Set has 82 stores, which average about 2,400 square feet. In November 2014, RET announced it would close its Smart Set chain and rebrand at least 70 stores. As of September 2015, currently, 35 Smart Set stores remain. This segment was likely EBITDA negative and will contribute to increased profitability.

Hyba: Hyba movewear offers affordable, on-trend active wear and yoga clothes. The segment can be seen as a lower priced competitor to Lululemon (NASDAQ:LULU). The concept was introduced at the end of 2013 and was rolled out in more Reitmans branded stores where it was well received. Due to the initial success of the brand and taking advantage of the available leases from the vacancy of Smart Set, Reitmans announced in August its intention to open 18 Hyba branded stores on October 8th. Assuming ~$1MM of average unit volume, the full year impact of Hyba should contribute $18MM in the first year. Assuming the first 18 units are a success, the Company expects to open ~100 units likely replacing closed Smart Set stores.

Per our channel checks, Canadian consumers are warming up to the brand, noting the quality is good as well as the price point vis-à-vis Lululemon and Lole. For instance, a pair of leggings, which costs ~$80 at Lulu and $90 at Lole, only cost $40 at Hyba with comparable if not better quality and similar styles. Finally, Mr. Reitman hasn’t made any outrageous comments or sold see-through leggings like Lulu! As budgets tighten, Hyba will gain share in the attractive athleisure wear market, although it may take four to six months to build brand recognition.

Other links of interest:

Hyba’s Rallying Cry For The Average Woman

E-Commerce: Led by Nathalie Belange, Reitmans’s e-commerce platform manages website shopping for all of its banners. The Company revamped its e-commerce strategy in FY13, bringing on a new divisional head whose departments assists with managing each brand and its social media presence, sharing PL responsibilities with the brand leaders of each respective banner. Previously, each brand managed its website presence separately. E-Commerce sales consist roughly ~5% of total sales or ~$46MM in Revenues. Per management, E-Commerce is a higher EBITDA margin business hence assuming 10% margins, E-Commerce contributes $4.5MM to $5.0MM in EBITDA per annum.

Valuation

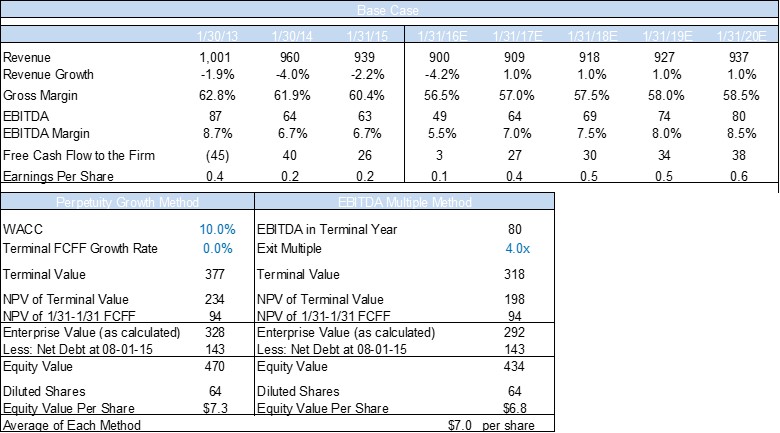

Base Case

The base case portrays a conservative scenario in which Reitmans stabilizes the top line and slowly improves gross margins. This scenario does not attribute a material impact to sales from Hyba, Addition Elle or additional cost cuts.

{kind=link}

Upside Case

The upside case portrays a more optimistic case in which the Company’s gross margins recover at a faster rate to ~60%. Note we do not model any major impact from Hyba.

Stress Case

For our stress case assuming margins continue to decline and the top line shrinks at greater than 2% per annum, we think the equity would trade at a slight premium to its net-net value to ~70% of tangible book value or $3 to $3.7 per share or ~15% to 25% downside.

Furthermore, a simple back of the envelope multiple analysis supports our valuation and risk/reward profile. Simply said, we easily think a deal could be consummated at or above $6 per share with a turn of leverage.

Catalysts

The following are potential catalysts, which could potentially lead to value realization:

- Continued SSS momentum: Same store sales have been strong at Reitmans, particularly in August. Sell-side estimates for SSS have continually been low, hence a SSS beat combined with stabilized or increased gross margins will likely lead to a re-rating. Furthermore, while the weak Canadian dollar negatively impacts margins, it leads to higher SSS as Canadians are inclined to purchase within Canada vis-à-vis crossing the border.

- Strong Hyba Acceptance and/or Continued Success at Addition Elle: On October 8th, Reitmans hosted the grand opening for its 18 Hyba stores, which took over leases from Smart Set. Hyba is well positioned as an athleisure brand, priced significantly below Lulu and Lole while carrying similar quality. It will, however, take some time for the brand to build recognition and may require a spokesperson or two signed on. Addition Elle continues to grow on the back of its popular Ashley Graham lingerie lines as well as partnerships with various retailers. Additionally, the Company continues to build a strong name in the plus sized fashion community with collabs with popular plus-sized fashion bloggers such as Nadia Abdelhosn.

- Take Private or Dividend Recapitalization: Reitmans currently trades for 2x EBITDA. Considering Management and Fairfax’s stake, a take private in the mid $6s would be an easy transaction assuming no further deterioration in gross margins. We believe the business could easily handle a turn of leverage, allowing it to return ~50% of the enterprise value to shareholders. We find a dividend recap as highly unlikely given Management’s conservative stance.

- More so wishful thinking, yet if the Company could pull an Oprah and persuade Marcus Lemonis to invest and take the helm then we have a 10 bagger.

- Stabilization of Gross Margins: If the Company is able to mitigate the gross margin impact and adjust pricing (which some retailers are), the story will re-rate given the massive GM miss from the last quarter. This is simply a case of “you can still be bad, but not that bad.”

Thesis Risks

- FX Gross Margin Headwinds: In 2015, Reitmans must implement discounts in order to maintain its top line. With FX pressures now significant, the Company will have to find further costs to cut as well as revamp its FX hedging program. Gross margins will remain low due to discounting and ongoing liquidation at Smart Set. While sentiment is already negative and Reitmans has been downgraded, estimates have not been changed with gross margins of ~60% for 3Q16 vs. 61.2% for 3Q15. Gross margins will likely fall between the 56% to 58% range.

- Working Capital Movement: Working capital must be watched as inventory is up YoY, and payables have somewhat increased. While the Company’s cash balances are fairly consistent year over year, if this process occurs or RET falls into financial difficulties, this could impact value severely as in a liquidation, inventory holds little value.

- Torrid Entrance in Plus Size: Torrid’s entrance in Toronto hasn’t affected Addition Elle stores per our channel checks given a different target market, fashion style and price point. Nonetheless, this is to be watched.

- Poor retail environment in Canada: Reitman’s low multiple prices is in a recession. Strong balance sheet also provides a buffer. We also believe a pair trade with a handful of Canadian retailers isn’t a terrible idea. SRSS is one potential name.

- Lack of Disclosure: RET does not disclose sales or SSS by brand and disclosure isn’t the best. This is similar to other family controlled entities.

- E-Commerce Decelerates: E-Commerce is currently ~5% of sales and has room to continue to grow. Nonetheless, each incremental quarter, SSS growth in excess of 50% will be harder to come by. On the bright side, E-commerce carries higher margins.

Conclusion

While Reitmans and retail in general can be classified as a low quality business, its valuation and cash generation are highly compelling. While the Canadian economy is undoubtedly weak and consumers often scale back spending, we suggest potentially looking at Sears Canada or a bucket of Canadian retailers on the short side as a hedge. Finally, low expectations and high skepticism have created a favorable setup in which any word of success will lead to a significant re-rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.